Equity release has become a popular way for people aged 55 or older to access additional funds from their property, which can then be used for a variety of reasons. Parents may help their children to purchase their own home, or simply enjoy greater financial freedom during retirement.

There are different options available when it comes to Equity Release, such as lifetime mortgages and home reversion, as discussed here:. It makes sense to consult with an expert such as Parachute Law before signing up for any scheme, in order to be sure that you are making the right choice, and that the process is carried out as efficiently as possible.

What You Will Need

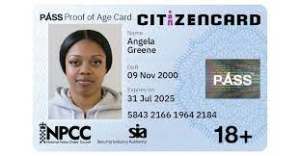

If you decide to go ahead with releasing equity from your property, you will need to provide certain documents. First of all, you must be able to present a photo ID to your advisor, which will enable the financial institution to verify that you are who you say you are. Such an ID can take the form of a current passport or driving licence, and it must match the address given on your property details.

You will also need to produce a building insurance schedule before the process may begin. This document will assure the value of your property at the time of completion, and should match the sum settled upon by your chosen lender.

Your lender will want to see evidence of a minimum of three month’s worth of council tax or utility payments for the property. Council tax payments are the preferred documentation here, and when it comes to utilities, choose something like your energy bill. A mobile phone bill, for example, won’t be eligible in this situation.

Of course, your lender will also want to see at least three month’s worth of bank statements, too. These statements must show your name, address and account number but you may redact transactions if you prefer.

Documents Relating To The Property

Don’t forget the title deeds to the property, and be sure that only your names are listed on this document. If there has been a divorce or bereavement that has changed the situation since the deeds were issued, you will need to remedy this situation with the Land Registry.

An occupier waiver form is another essential document. The signing of an occupier waiver form will be key to the equity release process. Being able to provide mortgage reference numbers and provider details will also help to speed up the route to equity release.

Finally, you will need to provide details of any specific scenarios that could affect your property or its value. If you have a leasehold on your property, you will also need to provide documentation relating to this. Similarly, if you have solar panels in place, you should have a receipt and Microgeneration Certification Scheme certificate, or be able to produce a copy of the panels’ lease.